ETL 1110-2-547

30 Sep 95

g E Xi % FX & g E Xi & FX

that of the continuous random variable. Having only a

MY

i

i

'

few values over which to integrate, the moments of the

2 FX

M Xi

performance function are easily obtained. A simple

i

and straightforward point estimate method has been

proposed by Rosenblueth (1975, 1981) and is

When the above expression is squared and multiplied

summarized by Harr (1987). That method is briefly

by the variance, the standard deviation term in the

summarized below.

denominator cancels the variance, leading to

(1) Independent random variables. As shown in

g X% & g X&

2

2

MY

Figure B-3, a continuous random variable X is

Var X '

M Xi

represented by two point estimates, X+ and X-, with

2

the two point estimates and their probability concen-

where X+ and X- are values of the random variable at

trations form an equivalent probability distribution for

plus and minus one standard deviation from the

the random variable, the two P values must sum to

expected value.

unity. The two point estimates and probability con-

centrations are chosen to match three moments of the

(2) Correlated random variables. Where random

random variable. When these conditions are satisfied

variables are correlated, the solution is more complex.

for symmetrically distributed random variables, the

The expression for the expected value, retaining

point estimates are taken at the mean plus or minus one

second-order terms is:

standard deviation:

E Y ' g E X1 , E X2 , ... E Xn

Xi% ' E Xi % FX

i

Xi& ' E Xi & FX

2 j M Xi M Xj

M2 Y

1

Cov Xi Xj

i

%

However, in keeping with the first-order approach, the

second-order terms are generally neglected, and the

expected value is calculated the same as for

independent random variables. The variance,

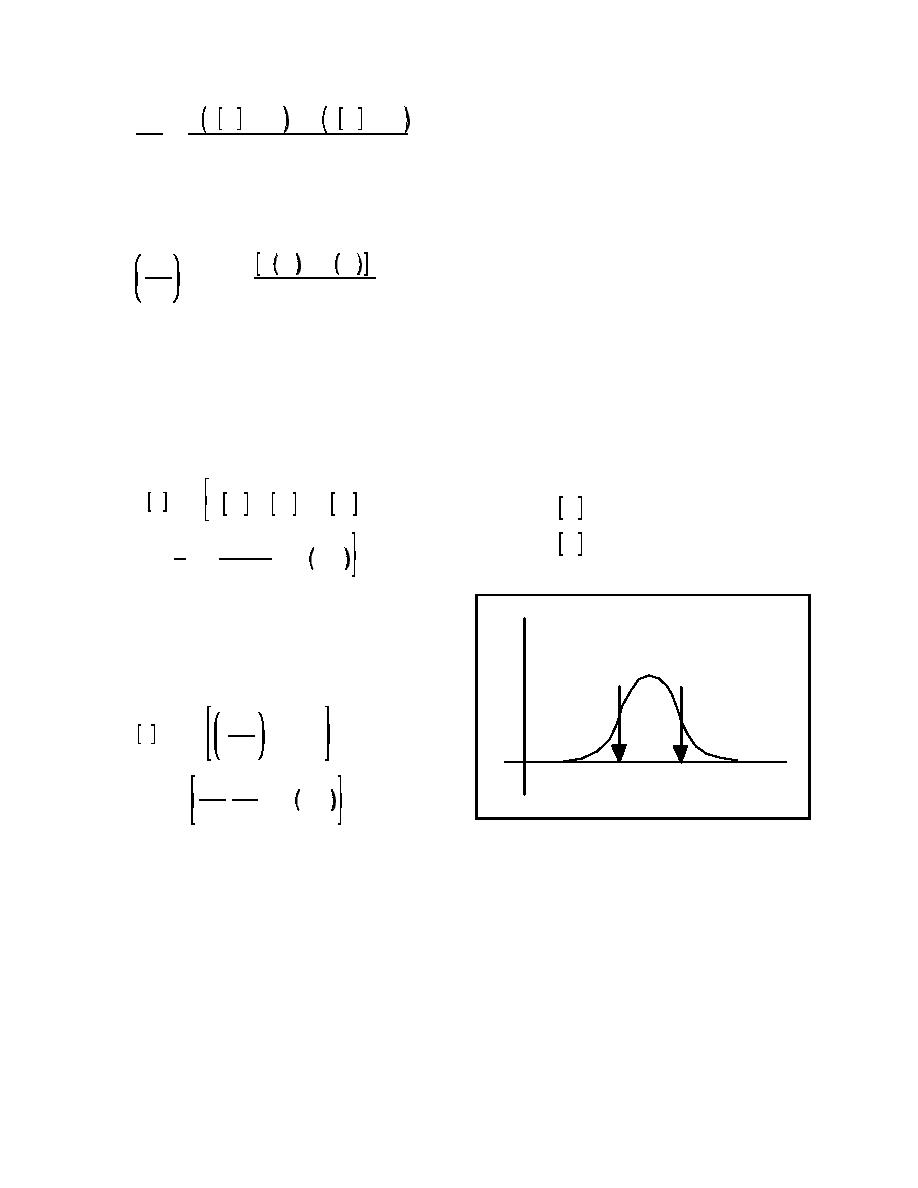

f(x)

P+

P-

however, is taken as:

Var Y ' j

2

MY

Var Xi

M Xi

x

x-

x+

%2j

MY MY

Cov Xi Xj

M Xi M Xj

Figure B-3. Point estimate method

where the covariance term contains terms for each

possible combination of random variables.

For independent random variables, the associated

probability concentrations are each one-half:

b. Point estimate method. An alternative method

to estimate moments of a performance function based

Pi% ' Pi& ' 0.50

on moments of the random variables is the point

estimate method. Point estimate methods are pro-

cedures where probability distributions for continuous

Knowing the point estimates and their probability

random variables are modeled by discrete "equivalent"

concentrations for each variable, the expected value of

distributions having two or more values. The elements

a function of the random variables raised to any

of these discrete distributions (or point estimates) have

power M can be approximated by evaluating the

specific values with defined probabilities such that the

function for each possible combination of the point

first few moments of the discrete distribution match

estimates (e.g., X1+ , X2- , X3+ , Xn- ), multiplying each

B-9

Previous Page

Previous Page